Estimate Process Parameters from Data

| In[1]:= | X |

| In[2]:= |  X |

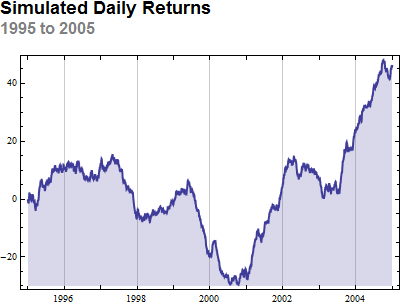

The following data is daily returns for a hypothetical stock simulated from a FractionalBrownianMotionProcess from January 1995 to January 2005.

| Out[2]= |  |

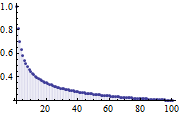

The estimated Hurst exponent suggests a long memory process.

| In[3]:= | X |

| Out[3]= |

This is exemplified by the CorrelationFunction of the estimated process.

| In[4]:= |  X |

| Out[4]= |  |