Heston Model

| In[5]:= |  X |

Define an ItoProcess corresponding to the correlated 2D Wiener process.

| In[1]:= | X |

Define a Heston model by SDEs driven by the correlated 2D Wiener process.

| In[2]:= |  X |

Simulate the model using a stochastic Runge-Kutta scheme.

| In[3]:= |  X |

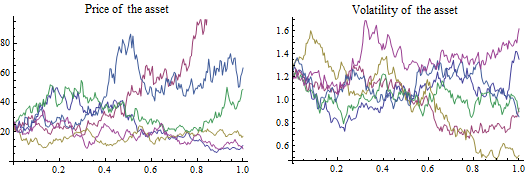

Visualize the sample paths.

| In[4]:= |  X |

| Out[4]= |  |