Convert Parametric SDE Processes to Equivalent Ito Processes

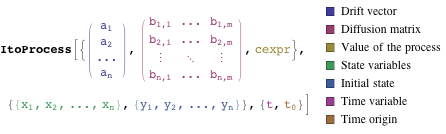

The canonical form of ItoProcess or StratonovichProcess in Mathematica encodes their defining SDEs  as follows.

as follows.

as follows. |

WienerProcess solves the SDE  , where

, where  is the standard Wiener process, also known as the Brownian motion process.

is the standard Wiener process, also known as the Brownian motion process.

| In[1]:= | X |

| Out[1]= |

GeometricBrownianMotionProcess solves the SDE  .

.

| In[2]:= | X |

| Out[2]= |

OrnsteinUhlenbeckProcess solves the SDE  .

.

| In[3]:= | X |

| Out[3]= |

CoxIngersollRossProcess solves the SDE  .

.

| In[4]:= | X |

| Out[4]= |

BrownianBridgeProcess solves the SDE  .

.

| In[5]:= | X |

| Out[5]= |