Stochastic Differential Equation for Exponential Decay

Define a stochastic process satisfying the Ito stochastic differential equation  . This models exponential decay subject to Wiener noise.

. This models exponential decay subject to Wiener noise.

| In[1]:= | X |

| Out[1]= |

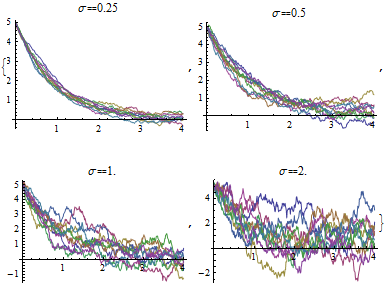

Simulate the process for different values of the variance parameter  .

.

| In[2]:= | X |

| Out[2]= |  |

The mean function of the process is independent of  .

.

| In[3]:= | X |

| Out[3]= |

This implies that the mean function coincides with the following deterministic solution.

| In[4]:= | X |

| Out[4]= |

Find the variance function of the process  .

.

| In[5]:= | X |

| Out[5]= |

Find the probability density function of the value of the process  .

.

| In[6]:= | X |

| Out[6]= |  |