Core Algorithms

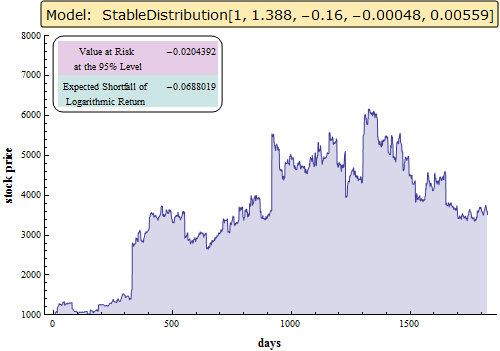

Use Stable Distribution to Model Stock Prices

Assuming daily logarithmic return of the stock market follows a stable distribution, simulate and visualize stock prices over a period of five years.

| In[1]:= |  X |

| In[2]:= |  X |

| Out[2]= |  |

| New in Wolfram Mathematica 8: Parametric Probability Distributions | ◄ previous | next ► |

| In[1]:= | X |

| In[2]:= | X |

| Out[2]= | |