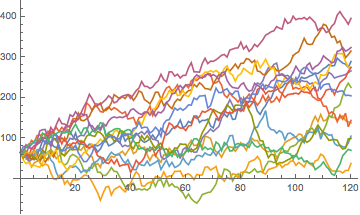

Simulate the Surplus Process for Insurance

Simulate the surplus process for insurance, given that the insurer's initial surplus is 65 and the total annual premium is 61.2, if the number of claims follows a Poisson process with mean 60 and the losses are distributed exponentially with mean 1.

| In[1]:= |  X |

| In[2]:= | X |

| Out[2]= |

| In[3]:= | X |

| Out[3]= |  |