Model Multiple Exchange Rates

Model and forecast multiple time series with vector‐valued time series processes.

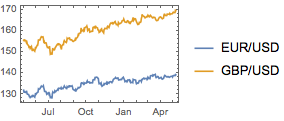

The exchange rates of EUR to USD and of GBP to USD as vector time series.

| In[1]:= | X |

| In[2]:= | X |

| Out[2]= |  |

Fit a vector ARMA model to the data.

| In[3]:= | X |

| Out[3]= |

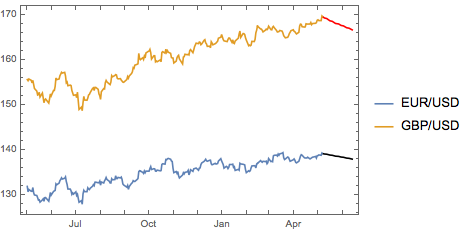

Forecast the exchange rates.

| In[4]:= | X |

| Out[4]= |

| In[5]:= |  X |

| Out[5]= |  |