Model the Conditional Value at Risk with an ARCHProcess

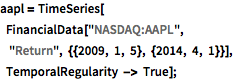

The returns of Apple stock from January 2009 to April 2014.

| In[2]:= | X |

| In[3]:= | X |

| Out[3]= |  |

Split the time series in two parts, and use the first part to find a model.

| In[4]:= | X |

| Out[4]= |

| In[5]:= | X |

| Out[5]= |

Fit an ARCHProcess to the first time series.

| In[6]:= | X |

| Out[6]= |  |

| In[7]:= | X |

| Out[7]= |

| In[8]:= | X |

| Out[8]= |

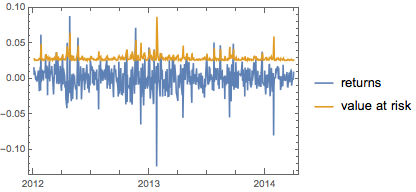

Find the conditional value at risk for the second part of the time series with significance level at 95%.

| In[9]:= |  X |

| Out[9]= |

Plot the second time series and its values at risk.

| In[10]:= | X |

| Out[10]= |  |