Constrain the Model Selection Set

TimeSeriesModelFit allows you to automate selection from a given family of models or from a given range of models, as well as to fix integration order or seasonality.

Generate data with small seasonality.

| In[1]:= |  X |

| Out[1]= |

Use TimeSeriesModelFit to automatically find the most suitable time series model.

| In[2]:= | X |

| Out[2]= |  |

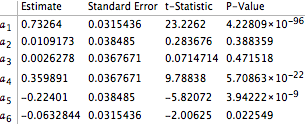

Based on variances of parameter estimators, the second and the third autoregressive coefficients are not significantly different from zero, suggesting possible seasonality of 4.

| In[3]:= | X |

| Out[3]= |  |

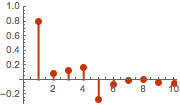

Confirm the seasonality guess with the plot of the sample partial correlation function.

| In[4]:= |  X |

| Out[4]= |  |

Restrict the search to seasonal ARMA family with seasonality of 4.

| In[5]:= | X |

| Out[5]= |  |

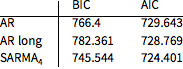

Compare with fitting longer autoregressive models.

| In[6]:= | X |

| Out[6]= |  |

Both the Bayesian information criterion and the Akaike information criterion favor the seasonal model.

| In[7]:= | X |

| Out[7]//TableForm= | |

| |