Moments of GARCH(1,1)

The value of a generalized autoregressive conditionally heteroscedastic process GARCHProcess has a heavy-tailed distribution with only a few finite moments of low order.

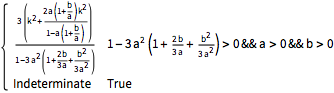

Fourth moment of a GARCHProcess with orders (1,1).

| In[1]:= | X |

| Out[1]= |  |

Define the function to extract moment finiteness conditions.

| In[2]:= |  X |

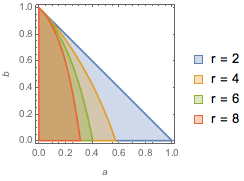

Visualize the parameter conditions for moments to exist.

| In[3]:= |  X |

| Out[3]= |  |

Values of the first few even moments for a weakly stationary GARCHProcess.

| In[5]:= | X |

| Out[5]= |  |

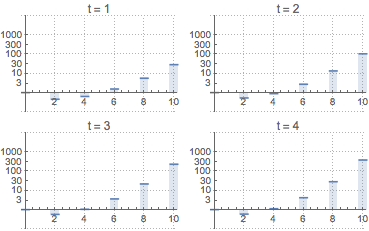

Compare to the values of the even moments for a non-weakly stationary GARCH with process initial values set to zero.

| In[6]:= |  X |

| Out[6]= |  |